This year has included a lot of comparisons back to 2014. That year was the year that grain prices declined after a multi-year run at historic highs, peaking in August 2012.

2014 was also the year that land values declined in reflection to the decline in grain markets.

Market Value 2014 vs 2024

The average Iowa corn price for the marketing year declined from $6.23 in 2013 to $4.51 per bushel in 2014. 2024 showed a similar outcome following a $6.09 average in 2023. Soybeans fell by more than $1 per bushel back then and by more than $2 per bushel in ’24 compared to ’23.

The average cost of production (per ISU) is actually within pennies per bushel for both corn and soybeans, comparing 2014 and 2024. Neither allowed for profit if one uses average costs and returns.

Those operators who can achieve below average costs and above average yield and/or price may turn some profit.

The time between 2015-2020 was a six-year stretch where “average” showed no profit on a monthly basis for neither corn nor soybeans.

As of this writing using the ISU averages, “average” corn has not shown a profit in 2024 while beans have shown slim profit, but now turning negative. There are high yielding fields in 2024 which will “bushel” their way to a profit.

Land Value Impact

Surveys show downward pressure on land values began during 2014 and stabilized by 2016 or 2017, then holding close to steady until 2021. Total downturn was 15-25% depending on what and where.

Remember that local farmers are the winning bidders at auction about 70-80% of the time and are often the 2nd final bidder as well.

Local farmers determine the land market most of the time. Investors are often a presence but may not engage in that final bidding push unless they have specific circumstances (i.e., adjacent location, 1031 exchange) or feel the property is priced competitively.

Following three years of excellent profit margins from 2021-23, farmers had a chance to solidify their finances. Many chose to decrease income tax liability by upgrading or expanding their line of equipment.

Some chose to also build working capital (paying taxes). The cash reserve becomes available for future use, such as a down payment on a land purchase.

Rapidly decreasing working capital reserves has become a common concern among bankers and ag economists in 2024. This means the pool of bidders decreases and those maintaining considerable reserves will become more cautious.

2024 Land Values (so far)

If you track the land market you’ve noticed a downshift in values, but some bell ringers are still occurring. Those tend to occur only in certain neighborhoods.

Overall, the land rally peaked in the 2nd quarter of 2022. Quarterly averages have traded mostly steady to lower since then but with several quarterly increases. 2024 has seen:

- 1st quarter: solidly higher from late ’23, average volume

- 2nd quarter: down, low volume

- 3rd quarter: steady with 2nd quarter, average volume

- 4th quarter: as of October 21st down from 3rd quarter

Recent trends are certainly a different story when comparing back to mid-2022. The two-year change from the high is in the 15% ballpark as measured in both $/acre and $/CSR2 on highly tillable farmland.

That change has accumulated over the prior 8 quarters, not just in recent months. If someone makes a statement about the land market being X% lower, be sure to ask “compared to when?”

Land Value Surveys

The most recent Iowa Realtors Land Institute survey measured opinions of change in land values from March 1st to September 1st. That survey showed all districts in Iowa ranging from -3.6% to -6.0%.

Our trade territory ranged from -3.6% in north-central Iowa to -5.0% in west-central Iowa. Their March 1st survey showed -2.1% to -4.7% in this region.

The annual change totals as much as nearly 10% lower. The Federal Reserve Bank of Chicago’s survey of banker’s opinion indicates only -3% in Iowa as of July 1st.

We’ve noted in the past that opinion surveys tend to lag reporting a market downturn. That is human nature, waiting for bad news to fully confirm itself.

Back to 2014 vs 2024

The earlier downturn was 15-25%. We’ve now seen a portion of that occur since mid-2022. If grain income can stabilize, we’ll see the land market follow suit.

The monthly average price of Iowa corn from 2015-2020 (72 months) was $3.50. Soybeans averaged $9.05. Land values were steady to lower.

The other 116 months since 2009 averaged $5.39 corn and $12.68 beans with rising land values. USDA’s price projection in their October report estimates $4.10 per bushel average corn price and $10.80 soybeans with record yields.

Conclusion

High yields at $4.10 and $10.80 may provide for a steady land market but probably not higher. Some areas in our region are not enjoying high yields and cannot “bushel” their way to profits this year. Those areas will likely see lower land values as caution and reduced working capital weigh in.

It seems likely that continued softening will occur in the land market. Volume of land for sale will play a strong role in value trends for each neighborhood.

Long-term, Iowa farmland appreciates by 4-5% annually, depending on the measurement period. Average crop yields appreciate by about 2% annually.

Farmland enjoyed great gains in value in 2021-22. It takes a downturn or long-term steady market to return to the long-term average. That is the current phase of the market.

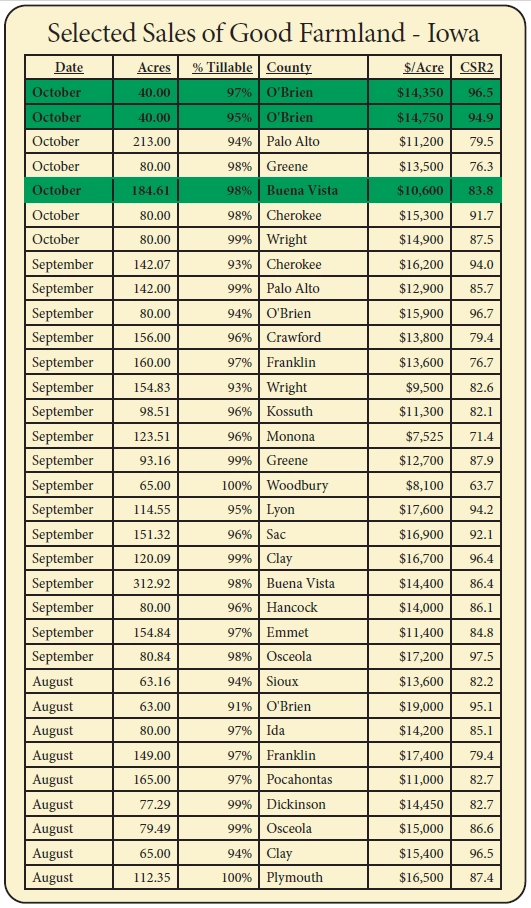

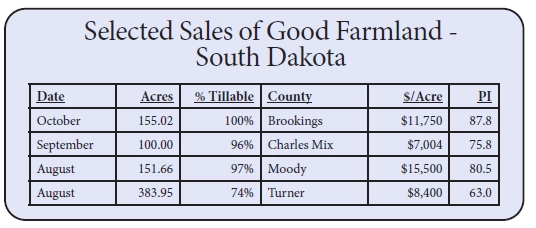

The following are two tables of selected “good” farmland in Iowa and South Dakota which have sold recently in the region. Stalcup-brokered sales are highlighted in green.