The market for Midwest farmland, especially prime Iowa farmland, is so widely covered during hot markets that you’re no doubt well aware of the major stories. For example, when a property sold for $25,000 last May, it was widely reported. Another parcel fetching $30,000 per acre last November caught even more attention.

I am always reminded of two age-old real estate axioms: “one sale does not make a market” and “location, location, location.” Sage reminders that will never become obsolete.

What we’re seeing…

Our land auction database covers the northwestern 25% of Iowa, plus surrounding areas. Focusing on Iowa farmland that is at least 85% tillable cropland with no other factors contributing significant value, we find the average parcel size offered during 2022 was 103 acres. The average transaction was $1.6 million, and the average value per acre was just over $15,500 per acre. Of these sales, about 20% hit $20,000 per acre or higher, while fewer than 10% were under $10,000. Each sale has its own story that goes beyond the $/CSR calculation.

Overall, land values peaked in the 2nd quarter of 2022, then stabilized in the 3rd quarter and slipped slightly in the 4th quarter. We noted a 3% drop in the 4th quarter average after quality is factored in. The famous $30,000 sale was part of the 4th quarter; however, with heavy sales volume, that sale barely affected the overall average.

As we near the end of the 1st quarter in 2023, we note that the total acres offered for sale in this region during the first three months are only slightly less than the past five years. Activity varies considerably by neighborhood. After factoring for soil quality, the overall average land value has been about steady with late 2022.

How about the surveys?

Iowa State University Extension’s annual survey reports findings as of each November 1st. This year, the survey was 17% higher for the entire state. Most counties in this region were about 20% higher. ISU also provides a chart that adjusts land values to 2015 dollars (an inflation adjustment). Today’s $11,411 state average adjusts to $9,088 in 2015 dollars. That’s a record, besting $8,854 inflation-adjusted in 2013. The 1970s topped at $6,384 inflation-adjusted in 1979.

Farm Credit Services of America releases a semi-annual update of land values based on 21 benchmark farms. As of January 1st, they showed 3.4% higher in the past six months with 12.9% higher year over year. This is not exactly comparing apples to apples with the ISU survey. Some of the difference is due to timing, and some is due to the survey method versus the benchmark method.

The Iowa Chapter of the Realtors Land Institute releases its semi-annual survey on March 29th, with values as of March 1st. Stalcup Ag Service participates in both the ISU and RLI surveys. The South Dakota State University Extension land value and cash rent survey will be released in early May.

Land Market Bubbles

On average, Iowa farmland doubles in value about every 15 years. During land booms, it may double in 3-5 years. Currently, the state average is double the 2010 value. Today’s averages are about 50% higher than five years ago.

Farmland rarely backs up much in value. Iowa farmland has had a pretty steady upward climb since statehood in 1846. The 2007-2013 ethanol-inspired boom was followed by a 15-20% decline from 2014-2016, then steady until late 2020. Outside of that setback and the crash of the 1980s, Iowa farmland has seen only a few years of minor declines since 1933.

Inflation and higher interest rates

Borrowers enjoyed extremely low interest rates over the past 15 years. That has changed now that the Federal Reserve is maneuvering interest rates in an attempt to manage inflation. Prime rate is 7.75%, the highest since 2007, which is a shock to the under-40 folks who’ve normally worked with rates at half that. Even older borrowers need to adjust after such a long period of lower rates. Actually, the daily weighted average over the past 75 years is about 6.4%, which includes the extreme rates of the 1980s.

Higher rates obviously raise the cost of renting money. This impacts residential properties quickly, since borrowers typically try to buy as much house as they can afford. Farmland is a little different since it is an income-producing property that is most often purchased as an add-on to an existing operation. Cash flow from the entire operation subsidizes the land purchase and may be strong enough to offset the effect of higher interest rates for the time being.

Banks and others have been advertising CD rates of 4% and higher. That will keep some money in the bank instead of chasing a 2-3% cash return in farmland. Of course, CDs don’t appreciate in value and, in fact, suffer erosion of purchasing power during inflationary periods.

What’s ahead?

Many family farms have grown to the extent where another parcel can be purchased and covered with the cash flow of the overall operation. Does that make it a sound investment? Since building a farming operation is a generational process, it does make sense over the long run if they can handle the cash flow requirements in the short term.

This does not mean that paying for $15-20,000 per acre land is easy. For example, if one were to borrow $15,000 per acre over 20 years at 6% interest, the payment would be more than $1,300 per acre. Lenders won’t approve that because cash flow from the property itself is insufficient. Obviously, one must either be able to put sizable cash toward the purchase or include more land as equity for a loan to spread the cost.

All-cash purchases are not necessarily the norm. For example, Farm Credit’s annual report shows growth in long-term mortgage loans but steady for production loans and intermediate-term loans. Mortgage loans account for nearly 62% of their total loans compared to 57% in 2019.

Considering that local farmers are the buyers of around 75% of land offered for sale and are most often the winning bidder and/or second bidder at auctions, they are the driving force behind land values. When farmers experience tighter cash flow for long enough and their cash reserves shorten up, they will push bids a little less and today’s results will become harder to achieve. We’ve talked with a number of farmers who would like to buy land but are waiting for some pullback in values.

Short term, softness in the land market could be expected at some point, but no one can exactly foresee the timing. We all understand that while the long-term trend line is upward, short-term realities always include ups and downs.

Bottom line is we believe there is too much equity in Iowa agriculture and too much optimism for the future of farming for land values to crash. Outside economic or geopolitical forces would need to force that to occur. However, some softness in values will likely occur at some point in the next few years, which many will see as a buying opportunity.

Foreign Ownership

Here’s another hot topic in the media. South Dakota is working on legislation limiting foreign ownership of farmland. Iowa does restrict foreign ownership to those with permanent residency (green card). Some at the national level are pushing for restriction of foreign ownership of farmland. It is an issue of national security, and it is also a local issue from a sociology standpoint.

Will foreign owners care anything about reinvesting locally? If you own land far away, do you send a donation to their local volunteer fire department, hospital, or food pantry? It would be appreciated.

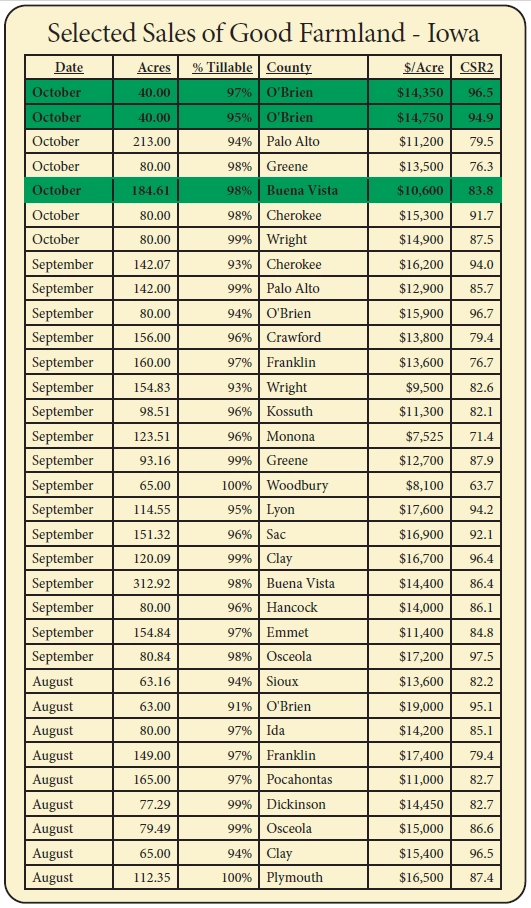

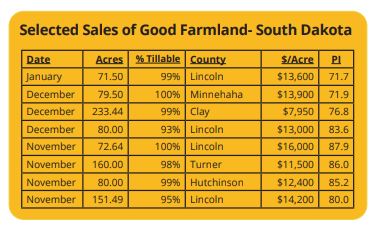

Following are two tables of selected sales of “good” farmland in South Dakota and Iowa which have sold recently in the region. Stalcup-brokered sales are in bold and highlighted in green. See page 5 for the Iowa sales table.