2023’s land market has rounded third and is heading for home. The 3rd quarter is in the books and we’re into the 4th quarter, which typically has the highest sale volume.

Our summary of sales in the 3rd quarter showed some weakness in mid to lower-quality farms while high-quality tracts showed mostly steady values. Each sale has its own story, of course, which may not fit the overall trend. We expect the general trend to continue as lower grain prices and higher interest rates make buyers a little selective in deploying capital.

Sale volume in the 3rd quarter was less than Q3 of 2021 or 2022, but considerably stronger than prior years. We note that the highest prices (both $/acre and $/CSR) occurred in the 2nd quarter of 2022.

Surveys

The most recent edition of the Realtors Land Institute semi-annual survey of broker’s opinions placed our trade territory at down 1-3% depending on region. This follows a decline of around 1% the prior six months. This basically amounts to the difference of a few bids at a public auction.

The Chicago Fed Ag Letter shows similar results with western and central Iowa at -2% for the 2nd quarter and steady to -1% for the prior year. That is a survey of banker’s opinions.

Previous Bull Runs and Pullbacks

After an exceptionally strong run-up from late 2020 to mid-2022, it is no doubt beneficial for the long-term health of the ag economy that land values take a pause.

From 2017 through Q3 2020, our database of highly tillable land sales showed an average of $8,850 with less than 4% variance over those 15 quarters. We then experienced seven quarters of skyrocketing land values, followed by now five quarters of steady to softer values.

A look back at the 1970’s shows a bull run lasting from late 1972 to late 1979 – a run of 30 quarters. That was followed by a collapse of land values which lasted most of 20 quarters in the early to mid-1980’s.

Another bull run in land values began with the ethanol era in late 2006. That was interrupted by the global financial collapse in late 2008 and early 2009, but resumed by mid-2010 through 2012. During that time frame, 20 of 25 quarters posted sizable gains in land values. That was followed by a stretch of steady to softer values in 20 of 30 quarters.

With this perspective, our recent bull run of seven quarters followed by five steady to softer quarters fits well.

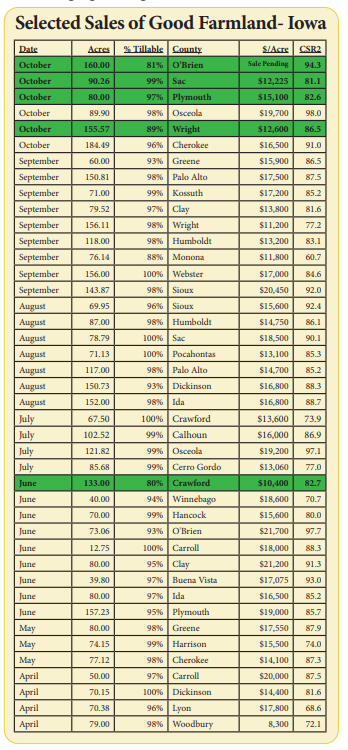

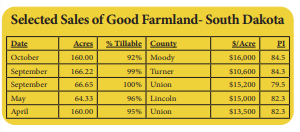

Following are two tables of selected sales of “good” farmland in South Dakota and Iowa which have sold recently in the region. Stalcup-brokered sales are in bold and highlighted in green.